Advertisement

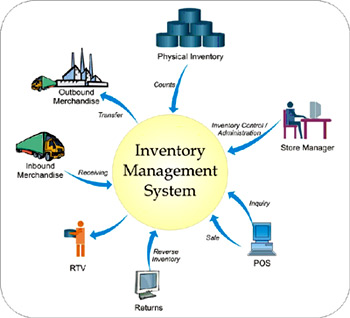

Inventory Management: – What is inventory control? In a lay man’s term – Its the control processes enables stockroom and supply managers to: Reduce time spent looking for inventory items. Prevent overstock and out-of-stock situations. Monitor item consumption. Increase accountability and prevent shrinkage.

No one has undoubtedly or correctly dated when inventory management arose. Nevertheless, inventory management was just about counting and keeping stocks records. The earliest evidence archaeologists have found of human counting things are ancient tally sticks dating far back 50,000 years.

Clay tokens found in Iran dating back over 4,000 years an interesting take on agricultural inventory; for example, to create a record representing two sheep, ancient inventory managers would select two round clay tokens with + signs baked into them. Of course, using large number of tokens for very large flocks would be impractical, so different clay tokens were used to represent various numbers of different commodities.

Inventory management developed steadily but slowly over many thousands of years. The development of accounting systems in ancient Greece and Rome had wide ranging implications for commerce as well as civil society.

Robust record keeping enabled ancient societies such as those in present-day Greece and Egypt to achieve feats of engineering that stand even today. Successful inventory management contributed to military victories as well as civic advancement; Roman strategy in the second Punic War involved an epic logistics effort to secure security of supply for Rome no matter how many battles the Carthaginians won.

At the end of 1880s, Herman Hollerith, an American inventor developed an electro-mechanical punch card tabulator.

The punch card allowed people to record many types of data, including inventory, by creating small holes in pieces of cardboard. This invention was leveraged by later inventors to develop the very first ordering system.

Customers in a store could fill out a punch card, the system would then read the punch card, send the information to the storeroom and someone from the storeroom would then bring the item to the customer. The system looked up items from a catalog and was able to manage the financial and inventory recording aspects of a transaction.

Retailers in the 1960s inspired by the earlier work with UV sensitive markings, developed a new way of managing inventory,the bar-code. There were a number of competing bar-code technologies until the industry adopted the ubiquitous Universal Product Code (UPC) bar-code symbology in the mid 1970s. The first UPC bar-code ever to be scanned was a 10 pack of Wrigley’s Juicy Fruit chewing gum at a supermarket in small town Ohio.

Although many businesses are only implementing inventory management software, technological advancements in the 1980s and 1990s spurred larger businesses to implement computerized systems. Because computing power was still very expensive, most small to medium sized business were left out in the cold. Around the turn of the century, the same kinds of advanced inventory tracking software became available to smaller businesses. Many early adopters also embraced spreadsheet applications and built their own inventory control systems.

Brief definition of common inventory control terms are given as:

– Lead or procurement time: The period of time expressed in days, week, or month etc. This is the time between the placement of an order and the receipt of order.

– Demand level: The amount required by sales, production etc usually expressed as a rate of demand per week, month or year. (This is the most important characteristic in inventory situation because it shapes the manner in which inventory problems are analyzed and solved. The demand pattern of an item may be deterministic (when it is assumed that the quantity needed over subsequent periods of time are known with certainty) or probabilistic (when the requirement over a certain period of time are not known but their pattern can be described by a known probability distribution)).

– Economic Order Quantity (EOQ) or Economic Batch Quantity (EBQ): This is a calculated ordering quantity which minimizes the balance of cost between inventory holding cost and reorder cost. It minimizes the total annual inventory cost.

– Buffer stock, minimum or safety stock: A stock allowance to cover errors in forecasting and lead time or the demand during the lead time.

– Maximum stock level: This is the amount expressed in units of issue above which the stock should not be allowed to rise . Its purpose is to curb excesses in investment. When this level is reached, it is a signal to defer or cancel outstanding deliveries, if any.

– Reorder level: The level of stock at which a further replenishment order should be placed. The reorder level is dependent upon the lead time and the demand during the lead time.

– Setup cost or production change cost: Is associated with the changing of materials, equipment and paper work and the removal of previous inventory for the production of a new product.

– Ordering cost: This includes all costs related to the placement and retrieval of an order.

– Purchasing cost: The variable cost per unit purchased and it includes raw material cost, labor and overhead costs, involved with the purchasing of a unit of product.

– Holding cost or inventory carry cost: The cost linked to the single unit being carried by an organization for a single unit time. It includes all of the following aspect: storage cost, handling cost, insurance cost, taxes or inventory depreciation and any cost due to breakage, theft and obsolescence.

– Shortage cost: This cost is associated to correcting the back order or the cost income due to sales being lost.

When we talk of inventory, we mean stocks held for purpose(s). A convenient classification of the types of inventory is as follows:

– Raw materials: They include materials, components, fuel etc used in the manufacturing of products.

– Work in progress: These are partially finished goods held between manufacturing stages.

– Finished goods: These are completed products ready for sale or distribution.

Over the years, certain models have been developed to support the efforts made in production and retailing to cut down inventory-related cost.

These models take into account the intricate peculiarities of production and retailing and show how inventory-related cost may be minimized when the rules of the models are adhered to.

The unifying goal of the models, and indeed goal of inventory control is to determine the optimal quantity of goods to order and the time to order

In business.com, inventory model is defined as a mathematical equation that enables organizations to determine the optimal quantity and frequency of ordering and keeping goods and services available to the customer without interruption or delay.

According to Business Dictionary.com, inventory model is a mathematical equation or formula that helps a firm in determining the economic order quantity, and the frequency of ordering, to keep goods or services flowing to the customer without interruption or delay.

According to Barrow’s Accounting Dictionary, inventory models are quantitative models designed to control inventory cost by determining the optimal time to place an order (or begin production) and the optimal order quantity (or production run). The timing of an order can be periodic (placing an order every x days) or perpetual (placing an order whenever the inventory declines to x units).

According to freelancer, since most of us use traditional way to record data, this may lead to loss of data and theft between employees of the company. Implementing inventory control would also reduce the working energy and workforce of the company thus increasing the profit margin of that certain company.

According to Serhii Ziukov on inventory management under uncertainty. Stocks are created to carry out the normal activities of the company. Proper and timely determination of the optimal inventory control strategy allows freeing a significant amount of of assets,frozen in the form of stocks, which ultimately increases the efficiency of resource use.

Advertisement

Even though there are literally millions of different types of products manufactured in our society,there are two fundamental decisions that one has to make when controlling inventory :- How large should an inventory replenishment order should be? and when should an inventory replenishment order be placed?

It has been widely determined after various analysis that an inventory model has to be developed for the smooth running in determining stock control in an organization.

REASONS FOR HOLDING STOCK

1. To ensure that sufficient goods are available to meet anticipated demand.

2. To absorb variations in demand and production.

3. To take advantage of bulk purchase discount.

4. To meet possible shortages in the future.

5. To absorb seasonal fluctuation in usage or demand.

6. To enable production processes to flow smoothly and efficiently.

7. As a deliberate investment policy particularly in times of inflation and possible shortage.

Stock represents an investment by the organization and as with any other investment, the cost of holding stock must be related to the benefits to be gained and to do this efficiently, the cost of stock must be identified in three categories:

- – Cost of holding stock.

- – Cost of obtaining stock.

- – Stock out cost.

INVENTORY MODEL

An inventory consists of usable but idle resources such as men, machines, materials or money. When the resource involved is a material, the inventory is called stock.

An inventory problem is said to exist if either the resources are subjected to control or if there is at least one such cost that decreases as inventory increases. Also the inventory control problem is the problem faced by a firm that must decide how much to order in each time period to meet demand for its products.

Roles Information Technology Advisors Play In Businesses

INVENTORY COSTS

The four costs considered in inventory control models are:

1. Purchase cost :It is the price that is paid for producing/purchasing an item. It may be constant per unit or may vary with the quantity produced/purchased. If the cost/unit is constant,it does not affect the inventory control decision. However, the purchase cost is definitely considered when it varies as in quantity discount situations.

2. Inventory carrying or stock holding cost.They arise from account of maintaining the stocks and the interest paid on the capital tied up with the stocks. They vary directly with the size of the inventory as well as the time for which the item is held in stock.

3. Procurement cost or set up cost: These include the fixed cost associated with placing of an order or setting up a machinery before starting production. They include cost of purchase, requisition, follow up, receiving the goods, quality control, cost of mailing, telephone calls and other follow up actions, accounting and auditing, etc. Also called ordered cost or replenishment costs, they are assumed to be independent of the quantity ordered or produced but directly proportional to the number of orders placed.

4. Shortage cost: These costs are associated with either a delay in meeting up with demands or the inability to meet it at all.

It follows from the above discussion that if the purchase cost is constant and independent of the quantity purchased, it is not considered in formulating the inventory control policy. The total variable cost is given by

Total variable inventory cost = Carrying cost + Ordering cost + Shortage cost However, if the unit cost depends upon the quantity purchased i.e., price discounts are available, the purchase cost is definitely considered in formulating the inventory control policy. The total variable cost in this case is given by

Total variable inventory cost = Purchase cost + Carrying cost + Ordering cost + Shortage cost

INVENTORY CONTROL PROBLEM

The inventory control problem cost is of three basic factors :

- • When to order?

- • How much to order?

- • How much safety stock should be kept?

Benefits of Inventory control:

- • Protects a company from fluctuations in demand of its products.

- • Keep a smooth flow of raw materials and aids in continuing production.

- • Checks loss of materials due to pilferage.

- • Minimizes the administrative workload.

- • Avoids duplication in ordering cost.

- • Facilitates cost accounting activities

TYPES OF INVENTORY CONTROL SYSTEM

1. Reorder level system: This is also known as two-bin system. It usually has three control levels and they include:

– Reorder level.

– Minimum level.

– Maximum level.

The usual replenishment order is the EOQ. The reorder level system results in fixed quantities been ordered at variable intervals dependent upon demand.

Example: The following data relate to a particular stock item. Normal usage for the item is 110 per day, minimum usage is 50 per day and maximum usage is 140 per day. Lead time/delivery time is 25-30 days, EOQ is 5,000. Using this information, calculate the various control levels.

solution

Reorder level = Maximum usage × Maximum lead time = 140×30 = 4200units

Minimum level = Reorder level – Average usage for average lead time

where Average usage = Normal usage = 110

Average lead time = (25+30)/ 2 = 27.5

Minimum level = 4200 – (110 × 27.5) = = 4200 – 3025 = 1175

Maximum level = Reorder level + EOQ – Minimum anticipated usage in lead time

= 4200 + 5000−(50×25) = 7950

2. Periodic review system: This is sometimes called the constant cycle system. In this system, stock levels for all parts are reviewed at fixed intervals (eg every fourth night) and replenishment order issued to bring stock back to predetermined level.

The replenishment order quantity is based upon estimate of likely demand until the next review period. The periodic system results in variable quantities been ordered at fixed intervals.

THE ECONOMIC ORDER QUANTITY MODEL

The EOQ is a relative basic model that enables organizations to determine the optimal order quantity and order point.

These are assumptions and conditions that have to be met to be able to implement the EOQ model.

ASSUMPTIONS OF A BASIC EOQ MODEL:-

– Demand has to be continuous, constant and known(deterministic).

– Replenishment is constant and known.

– Lead time has to be zero or at least constant and known.

– For each order, ordering, setup and holding cost are incurred.

– All customer demand has to be satisfied, therefore no shortages are allowed.

– Purchasing prices must be constant and independent from order quantity and time.

– No inventory in transit is allowed, the delivery cost has to be included in the purchase price.

– All ordered inventory items has to be independent.

– Unlimited capital must be available.

– Planning period has to be infinite.

VARIABLES OF AN EOQ MODEL

D = Annual demand of unit

K = Ordering or setup cost.

Q = Optimal order quantity.

no = Optimal order cycle.

to = Optimal order time.

H = Holding / Carrying cost.

T = Optimal total cost.

ROPu = Reorder point (units).

ROPt = Reorder point (time).

qu = Quantity of units in inventory cycle.

SS = Safety stock.

EOQ is the simplest type of inventory model that occurs when demand is constant over time with instantaneous replenishment and no shortage. The highest level of inventory occurs when the order quantity is delivered.

Delivery lack is assumed a known constant. The inventory level reaches zero level time unit after the order quantity is received. The smaller the order quantity, the more frequent will be the placement of the order.

However, the average level inventory held in stock will be reduced. On the other hand, larger order quantities indicates longer inventory

Advertisement